A republished blog post from 4 June 2018 warning about some of the history and dangers of the planned cashless society.

Following the widely reported european failure of the VISA payments system last weekend, I hastily compiled this 'Twitter Moment' in order to help bring about a wider awareness and attention to the issues surrounding the moves being taken against the use of cash by governments, financial institutions and businesses over the past few years.

Friends over at Transnotitia responded by asking me to write a blog about this and other issues I tweet about regarding the future of finance and money. So here I present a compilation of information which may take quite some time to absorb. It's not intended to be read in one go, but to be used as a reference that will hopefully provide more than enough knowledge and information to help understand and educate others to certain dangers related to The Cashless Society ahead of us.

Since originally publishing this we have seen:

- Central Banks openly working together to create and push-out digital currencies

- Crooked IMF chief Christine Lagarde take over from Mario Draghi at the ECB.

- A crisis (corona virus pandemic) being used to shill for Central Bank Digital Currency (CDBC)

- Positive Money, founded by Ben Dyson, working in co-operation with his new employers The Bank of England, where he plays an important part of the Digital Currencies team.

- The World Health Organisation (WHO) saying that using cash is spreading the virus! (Whilst of course, staying silent on technology like McDonalds touch-screens of course!) despite the BIS themselves shortly after the Covid panic stating the risk of infection is minute from notes and they are safe.

- The continuing further erosions of our natural-born rights through government restrictions and decrees.

- A new environmental crisis being manufactured to make a grab at further resources (Extinction Rebellion/XR) into the hands of big-global centralised institutions to be funded by an unlimited supply of credit from central banks and globalist institutions.

A brief history of Panic

These are some key-events in recent living-memory which describe some very important events around finance, banking and cash.

2008 Global Bail-Out

A decade ago governments around the globe bailed-out their bankrupt financial institutions with newly-created debt loaded onto taxpayers in order to quite literally save the world - if you agree that 'the world' means the greedy banksters who ended-up getting their undeserved performance bonuses (unless they worked for Lehman Brothers or Bear Stearns). People around the world went through the full range of emotions as they suddenly had to deal with a housing collapse, mass-unemployment, recession etc in-addition to the fiscal belt-tightening so-called 'austerity' cutbacks in public financing that were imposed.

The masses in bailed-out countries were definitely not happy with this (and the subsequent consequences) so The Establishment knew that they would have to try a different solution to a bail-out the next time a crisis came around.

- Timeline For “Bail-In” Of G20 Banking System

- BoE Says G20 Nations To Enact Bank Deposits Theft Within 12 Months

2013 Cyprus Bail-In

In the spring of 2013, the appropriately-named governor Panicos of The Central Bank of Cyprus was forced to do the unthinkable and over a bank-holiday weekend. Cash withdrawals were limited to €100, depositors with under €100,000 faced a 'hair-cut' whilst depositors with over €100,000 were set to lose at least half of their money, if not all - a so-called bail-in.

Despite the now memorable reassurance of European Central Bank (ECB) Head Mario Draghi a year earlier that "the ECB is ready to do whatever it takes to preserve the euro", many around the world, especially in the European Union and eurozone became acutely aware that their money was no longer safe in the bank. If it could happen in Cyprus, it could happen anywhere, so it's unsurprising there that there were headlines about alternatives to (our fiat-)money like this:

Last year The Bank of Cyprus re-listed in London. Today there are Greeks Suing Cyprus for Lost Millions in Bank “Bail-In”. As for Panicos, he recently wrote Failing banks, bail-ins, and central bank independence: Lessons from Cyprus.

On January 1st, 2016 new bail-in legislation came into effect which proclaimed the end of taxpayer-funded bail-outs:

- EU enters brave new world of bank bail-ins

- EU calls time on 'too big to fail' with bank bail-in laws

These are just a handful of other countries that followed suit and implemented similar laws:

- G20 Governments All Agreed To Cyprus-Style Theft Of Bank Deposits … In 2010

- Growing Political Deception On Bank Deposits Theft

- Federal Reserve Says Bank Bail-Ins Coming To The USA

- New Zealand Banks “Pre-positioning” For Cyprus-Style Bail-In

- Australian Banks “Welcome” Cyprus-Style Bail-In Plan

2015 Greece Votes Oxi!

The long-suffering people of Greece voted in a new leftist political party Syriza on an anti-austerity platform. Leading the charge against the eurocrats was the flamboyant pro-European federalist finance minister Yanis Varoufakis who was mercilessly side-lined and ridiculed by his northern European opponents lead by Germany.

After months of fruitless discussions, he and his party put out a referendum to accept or reject the latest bail-out scheme being offered. The response from 'The Troika' in the run-up to the vote was swift and the country was immediately thrown into chaos. The government caved-in to Troika demands regardless of the referendum result and the rest is history as even worse conditions were imposed on the people of Greece for their impudence (and also as a warning to France, Spain and Italy who were having their own fiscal problems).

This was a perfect example to people around the world of the levels that a government and central bankers will sink-to in order to protect the financial oligarchy and its interests.

- 28 June (BBC) Greek debt crisis: Banks to stay shut, capital controls imposed

- 28 June (NYT) Greece Will Close Banks to Stem Flood of Withdrawals

- 5 July “Oxi”: A Historic Greek Vote Against Austerity

- 5 July (Reuters) Greeks defy Europe with overwhelming referendum 'No' - Note that they 'defy europe', not the EU/ECB, an often-repeated conflation and piece of word-magic. (Just as Brexit means 'The UK is leaving Europe'!)

- 10 July (NYT) In Athens, Greeks Wonder Whether Tsipras Folded or Restored Dignity

- 10 July (DN) Greece Submits Bailout Plan with Harsh Austerity Measures

- 21 June 2017 (Mint Press) How Greece Became A Guinea Pig For A Cashless And Controlled Society

- 17 December 2017 (Ekathimerini) Cash still king for the majority of Greek consumers, employers

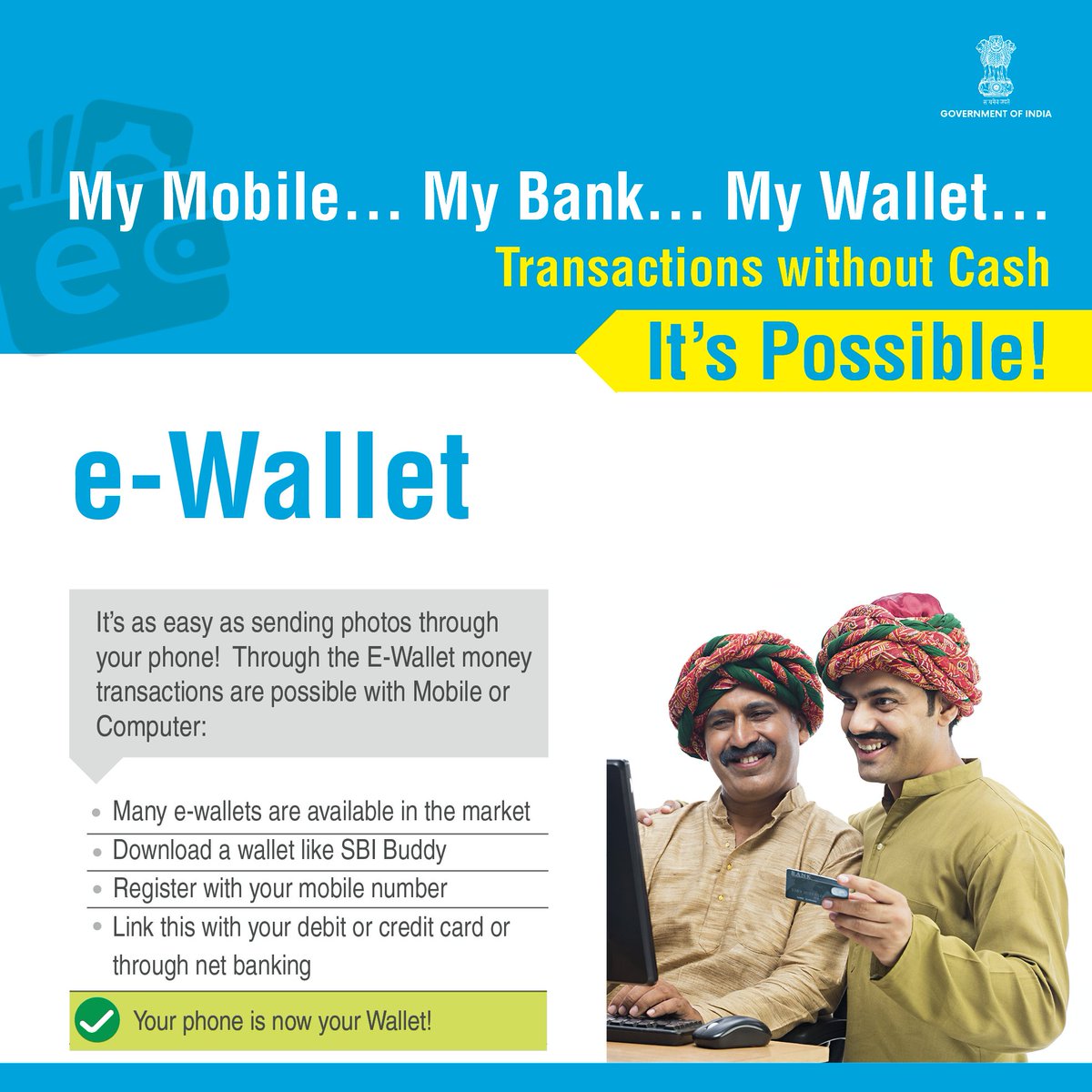

2016 India's Demonetisation

On 8 November 2016 India's demonetisation was announced. The global reaction - as with Cyprus - was once again of shock once-more stunned people saw that the government of the largest democracy in the world (~1.4 billion people) and its central bank can collude together and decide in secret to invalidate all of its printed banknotes if it so desires and there's nothing at all that a citizen can do about it!

By 28 November during the inevitable and on-going chaos, the under-fire Indian Prime Minister Narendra Modi tweeted 'Transactions without Cash - It's Possible!' whilst his government was seemingly making up the rules as they went along.

The situation is described in vivid detail by Jayant Bhandari who was there on-the-ground, a must-see:

Was it a success or massive blunder? The jury is still out for some - India's government trumpets it as a great success - but on the evidence presented in Jayant's video, they couldn't have done a worse job. The origins of the demonetisation fiasco have been described in an excellent blog post by Norbert Häring: "A well-kept open secret: Washington is behind India’s brutal experiment of abolishing most cash".

The following year a story reported that read "Paytm has said its e-wallet service has more than 200 million clients in India." (1/7 of India's population) but it's been reported that most of the people of India had switched back to cash. Note: Alibaba owns Alipay, one of the biggest Chinese cashless payment providers with 520 million users. Isn't it a national security issue for Indians?

Keeping Your Money Safe

If you've read this far, you should be aware that YOUR MONEY IS NOT SAFE IN A BANK! Your 'deposit' is legally a loan to the bank, and you're the last in the queue to get your money back should the bank fail.

So what can you do to protect your hard-earned savings? I'm not a financial advisor - so take this advice at your peril - but in practical terms, these are the simplest things:

- Take your money out of the bank as cold, hard, physical cash, leaving a minimal amount for monthly expenses. Keep the receipts (as evidence for when the taxman comes knocking) and of course pray that there's no demonetisation coming any time soon.

- Put your money in a stockbroker/share-dealing/gambling account because unlike the bank, they must maintain a separation of client funds. Some gambling/gaming sites even offer a free debit card you can use with your betting account.

- Save your excess savings in the form of gold coins - over the long term gold preserves its physical cash value, and can even out-perform cash in countries with an unstable currency. Gold coins are standardised, internationally recognised, easy to store and transport, and are free of tax in many countries and are compact in terms of price/weight ratio.

- If you have a large amount of savings, spread the money around accounts at different banks so that they are covered by 'deposit protection'.

- Do nothing. Trust your government's pronouncements and financial institutions 'Deposit Protection Scheme' and hope that it will work when the next crisis hits.

- Don't keep any money - buy things which can serve as a store of value and will provide some personal fulfilment and enjoyment, e.g. an allotment where you can grow your own vegetables. Or a vintage bicycle or piece of art - whatever!

- Model yourself on Mr T, buy and wear as much gold jewellery as possible. You will be able to easily move around and travel across borders without much hindrance, although the EU is cracking down on it.

Going Cashless

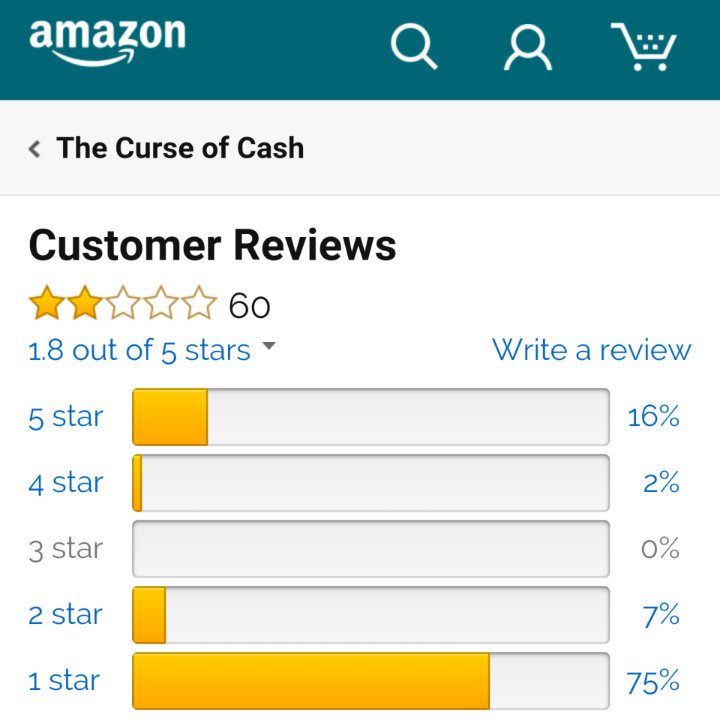

The Curse Of Cash

In late-2016, whilst angling for a top-job in the coming administration of Madam President, the so-called economist and defender of the usurocracy Ken Rogoff published the book "The Curse Of Cash" to widespread derision:

Rogoff's response to the comments and reviews. was cynical - it was more about 'fighting crime'! By the end of January 2017 he stopped tweeting after signing-off with Kenneth Rogoff: Why we need a 'less-cash society' in an article for the World Economic Forum (WEF), a public mouthpiece for the global Davos 'elite'.

Apple

In 2016 around the time of India's demonetisation Apple CEO Tim Cook stated "We're going to kill cash. Nobody likes to carry around cash." A year later Apple Pay Cash was announced - a deliberate conflation of language to confuse folks as to what (physical) cash is, and of course to help usher in the cashless society. This year we have the headlines continuing with Apple CEO Tim Cook wants to end money — and everyone working in financial technology should be paying attention where Cook is quoted as saying "Apple's CEO says he hopes to be alive to see the end of money."

Sweden

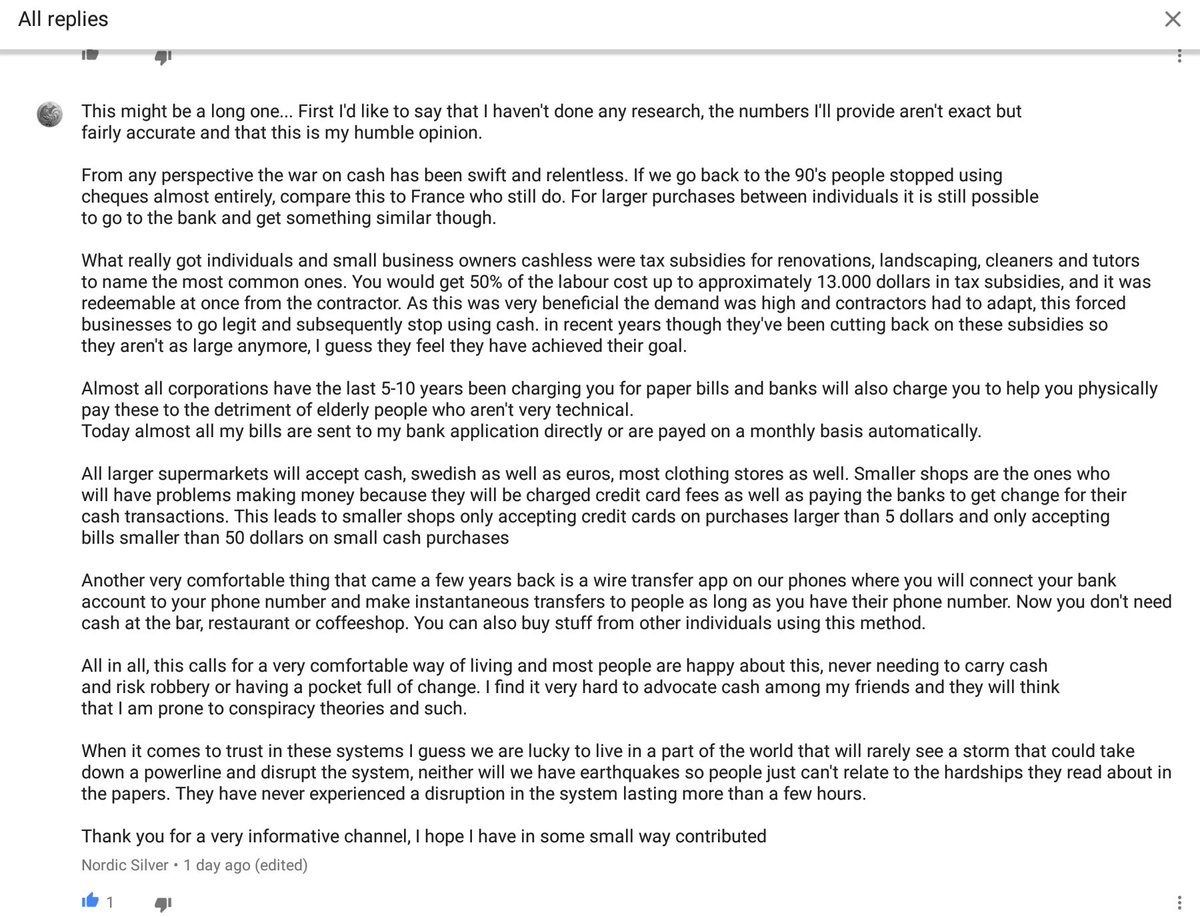

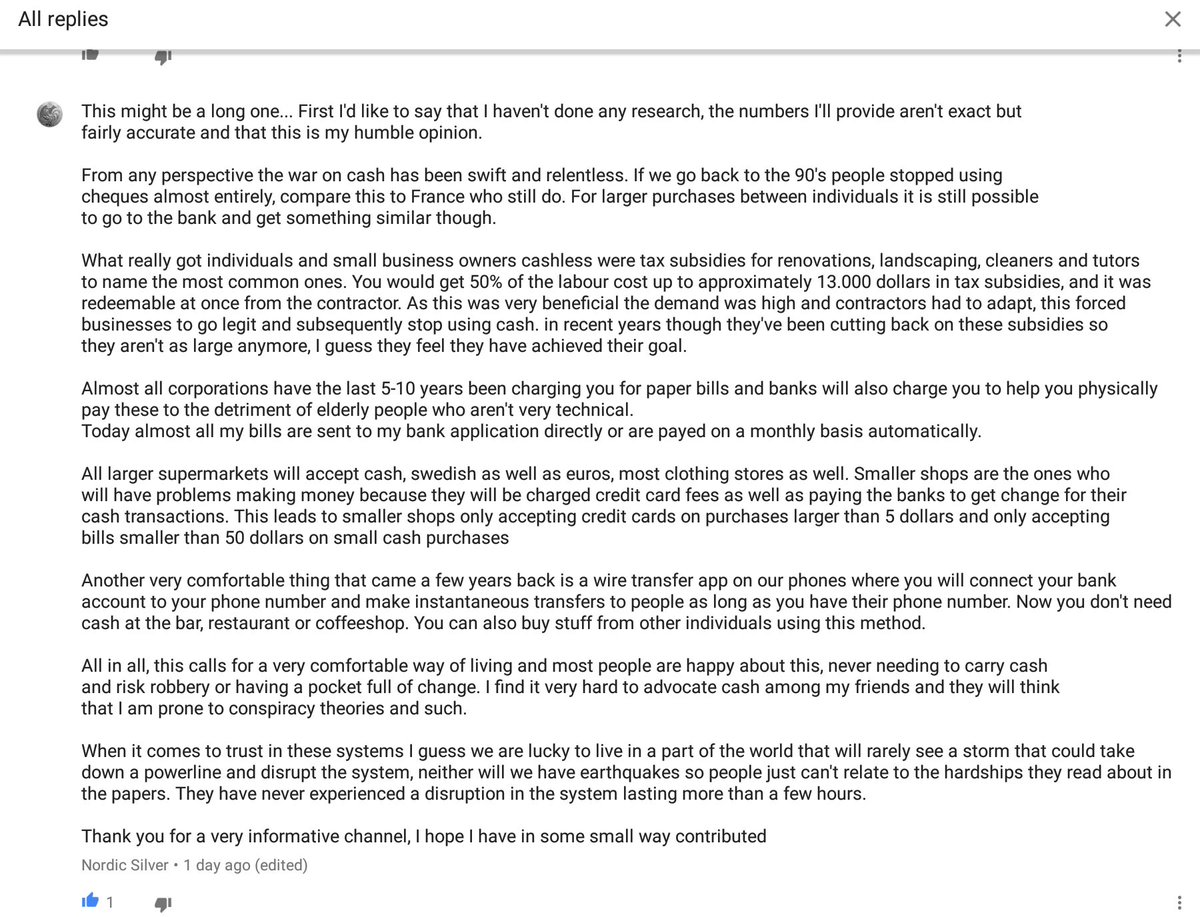

It is important to watch what occurs in Sweden to understand the future of cash and money. Sweden is at the forefront of the elimination of physical cash and cash transactions in The West. Having lived there 2011-14 I have much experience of it and last year I discussed it in a podcast about "Paper and Plastic Currencies & The Cashless Society" with Smaulgld

I explain that what Sweden did, unlike India, was to remove from circulation the smaller coins instead of large banknotes such that the lowest-value coin circulating was equivalent to 10 cents, forcing people to use cards to save money due to the rounding-up of figures (Swedish Rounding) at the till when shopping. This was an interesting and detailed comment by a Swedish listener about how Sweden became so cashless:

(Cashless Sweden comment - download image)

{kind=link}

An instant person-to-person payments mobile application called Swish was launched in Sweden in 2012 to some fanfare and has since grown rapidly in popularity.

A new range of banknotes (designed by the US Dollar printing family-firm monopoloy Crane Currency who had happened to buy Sweden's Tumba Bruk) meant demonetisation and exchange of old notes for new.

Old Woman In Sweden Becomes The Latest Victim of the War on Cash:

- From First on Cash to First Cashless – Sweden’s digital economy, is there a downside?

- Sweden could stop using cash by 2023

EU

- 4 May 2016: (ECB) ECB ends production and issuance of €500 banknote - '...decided to permanently stop producing the €500 banknote and to exclude it from the Europa series, taking into account concerns that this banknote could facilitate illicit activities...'

- 27 January 2017: (Zerohedge) Europe Proposes "Restrictions On Payments In Cash"

- 27 February 2017: (EU) EU initiative on restrictions on payments in cash

- 7 July 2017: ESTA, the Association of Cash Management Companies - Report concludes that cash does not play a major role in terrorist funding. Anonymity that cash provides is not critical to terrorists. ESTA speaks out against cash payment limitations in Europe whereas the results of the EU public consultation are now available

- 7 August 2017 ECB Board Member Yves Mersch: "As to the often stated link between cash and illicit payments, there is no evidence." Yves Mersch: Central banking in times of technological progress

- The use of cash by households in the euro area

- 10 December 2017: (Wolf Street Blog) A New Stealth Attack in EU’s “War on Cash”

China

Earlier this year China Uncensored published a video China Is Getting Rid of Cash which detailed how China now leads the world in cashless payments.

The Future of Cash

Innovations about how we use money are being developed leading to a convergence of new technologies and computer networks and software which will have a serious impact on our societies going forward. Managing personal identity in the digital world whilst eliminating it from the physical one is at the heart of it.

Distributed Ledgers

What enthusiasts call Blockchain or (central banks call) Distributed Ledger Technology (DLT) is mostly still in the early stages of being experimented with by governments and financial institutions to develop digital cash and asset management products.

Blockchain is a non-centralised, distributed network database that maintains a continuously growing list of ordered records (so-called 'blocks' which joined together which form a chain) duplicated and shared by each participating member of the network. It was first developed to support the bitcoin crypto-currency and the many digital crypto-currencies which have adapted and evolved from its original software codebase. Other applications that are in the finance arena are now being proposed and discovered in areas where global verification of data and proof of the validity is required. For example:

- World Economic Forum (WEF) - Realising the Potential of Blockchain

- The EU has a Blockchain Technologies Policy

- The UK's Financial Conduct Authority reveals next round of successful firms in its regulatory sandbox (Why should a financial regulator be doing this?)

- 8 June 2018 (WEF) video When is blockchain right for business? Skeptics and supporters alike lack the tools to assess the political, security and environmental implications of the technology and digital currencies.

- 8 June 2018 (PYMNTS) Mastercard Seeks Blockchain-Based Payment Verification Patent The company has filed for more than 35 patents in blockchain technology.

- 11 June 2018 (Better Than Cash) The Future of Supply Chains: Why Companies are Digitizing Payments New report underscores benefits of shifting from cash to digital payments in corporate supply chains

However despite the promises, there are some serious hurdles to overcome with blockchain as former software entrepreneur, now hedge-fund manager Erik Townsend of MacroVoices points out in his 17-page paper blockchain debunked.

In 2015 an in-depth interview with Harald Malmgren, an economist, veteran political 'fixer' and former US presidential advisor to multiple administrations was published under the title of "Cash as a Policy Tool ". It is a highly insightful interview which described from a technocratic and institutional perspective how cash is used and the US & Europe are developing cashless systems and why. He writes (my emphasis-added):

Banks in the US and Europe are trying to develop a cashless transactions system. The concept is to establish a comprehensive ledger for a business or a person that records everything received and spent, and all of the assets held – mortgages, investment portfolios, debts, contractual financial obligations, and anything else of market value including pleasure boats, automobiles, and other machinery. There would be no need for cash because the ledger would tell you and anyone you were considering a transaction with how much is available and would be transactable at any specific moment.

Central banks and governments would inevitably encourage even further consolidation so that all significant financial flows and all debts and assets could be monitored in real time, enabling policies and regulations to be adapted to the realities of daily life.

Cash is problematic to banks. It is expensive to manage, hard to take from customers and, worst of all, it is a possible gaping wound, if a bank run occurs. In a world without cash, customers would be forced to remain within the banking system, where all sorts of fees can be discretely and quietly shaven off millions of accounts

Governments would very much like such ledgers to exist because they could view everything that is taking place financially in real time, including ability to evaluate net worth, patterns of spending and of earned and unearned income, and of course, an instant assessment of all taxable activities. Governments would be able to gauge overall economic activity in real time, no longer needing to wait for months the collection of revenues and sales of businesses and surveys of consumer spending.

Note that Harald Malmgren mentions Blythe Masters who is on the board of ID2020.

June 4, 2018 - Remarks of Commissioner Rostin Behnam at the BFI Summit

“Fostering Open, Transparent, Competitive, And Financially Sound Markets” United Nations Plaza, New York, NY (as with Harald's interview, this really is a must-read):

The work of this summit could not be more vital. We are literally discussing a new world. Just as the founders of the United Nations spoke with optimism in 1948, so we may be hopeful about the future. Anything is possible. With your wisdom and guidance, we can transform this world into something wonderful. But in every transformation, there is the possibility that progress won’t march forward in the straight line we as optimists tend to envision. If we are not thoughtful, if we do not remain ever diligent to the movements within the transformation, we may unleash corruption, criminality, and division on a greater scale. Blockchain could become a source for repression and totalitarianism. The work before us is daunting and difficult. But, the rewards could be amazing and game changing. Our cooperation could heal the divisions that torment our world as we confront tragedy throughout our torn planet.

But virtual currencies may – will – become part of the economic practices of any country, anywhere. Let me repeat that: these currencies are not going away and they will proliferate to every economy and every part of the planet. Some places, small economies, may become dependent on virtual assets for survival. And, these currencies will be outside traditional monetary intermediaries, like government, banks, investors, ministries, or international organizations.

We are witnessing a technological revolution. Perhaps we are witnessing a modern miracle.

I started by mentioning the late Secretary General, Dag Hammarskjöld. At a dinner in 1957, he said that “the work for peace is basically a work for the most elementary of human rights: the right of everyone to security and freedom from fear.”

Blockchain is more than technology: it is an advance that reaches out into every aspect of life. We could use Blockchain to address the most basic, the most primal problems on our planet: corruption, income distribution, poverty, food, and health care. And, the fear billions of people experience everyday as they try to survive.

As a young child, I would come to this building in search of solutions to the problems of the world. Now, today, we may have found one of those solutions – bigger, bolder, more comprehensive, and more effective than anything imagined before.

Central Bank Digital Currency/Cash

- March 2018 (The Bank for International Settlements) Committee on Payments and Market Infrastructures Markets Committee Central bank digital currencies

- China’s central bank is developing its own digital currency, even as it bans bitcoin and private cryptos

- 18 May 2018 (Bank of England) Broadening narrow money: monetary policy with a central bank digital currency

- 30 May 2018 (Bank of England (staff)) Would a Central Bank Digital Currency disrupt monetary policy?

- 16 January 2017 Digital Base Money: an assessment from the ECB’s perspective

- Positive Money DIGITAL CASH: WHY CENTRAL BANKS SHOULD START ISSUING ELECTRONIC MONEY

- Federal Reserve (St Louis) The Case for Central Bank Electronic Money and the Non-case for Central Bank Cryptocurrencies

- Deutsche Bank Why would we use crypto euros? Central bank-issued digital cash – a user perspective

- Israel central bank mulls issuing digital currency for faster payments

- Norway's Central Bank Mulls Digital Currency as Cash Use Declines

- Central Bank Digital Currency and the Future of Monetary PolicyMichael Bordo and Andrew Levin May 2017

- Bank of Canada Central Bank Digital Currencies: A Framework for Assessing Why and How

- Bank of Canada Learn more about three areas of our ongoing work on digital currencies and financial technology

- Central Bank of Malaysia Central Bank Digital Currency: A Monetary Policy Perspective

- Swedish Central Bank Explores E-Krona Digital Currency

Digital Identity

(Image: USAID's 2018 Digital Development Awards)

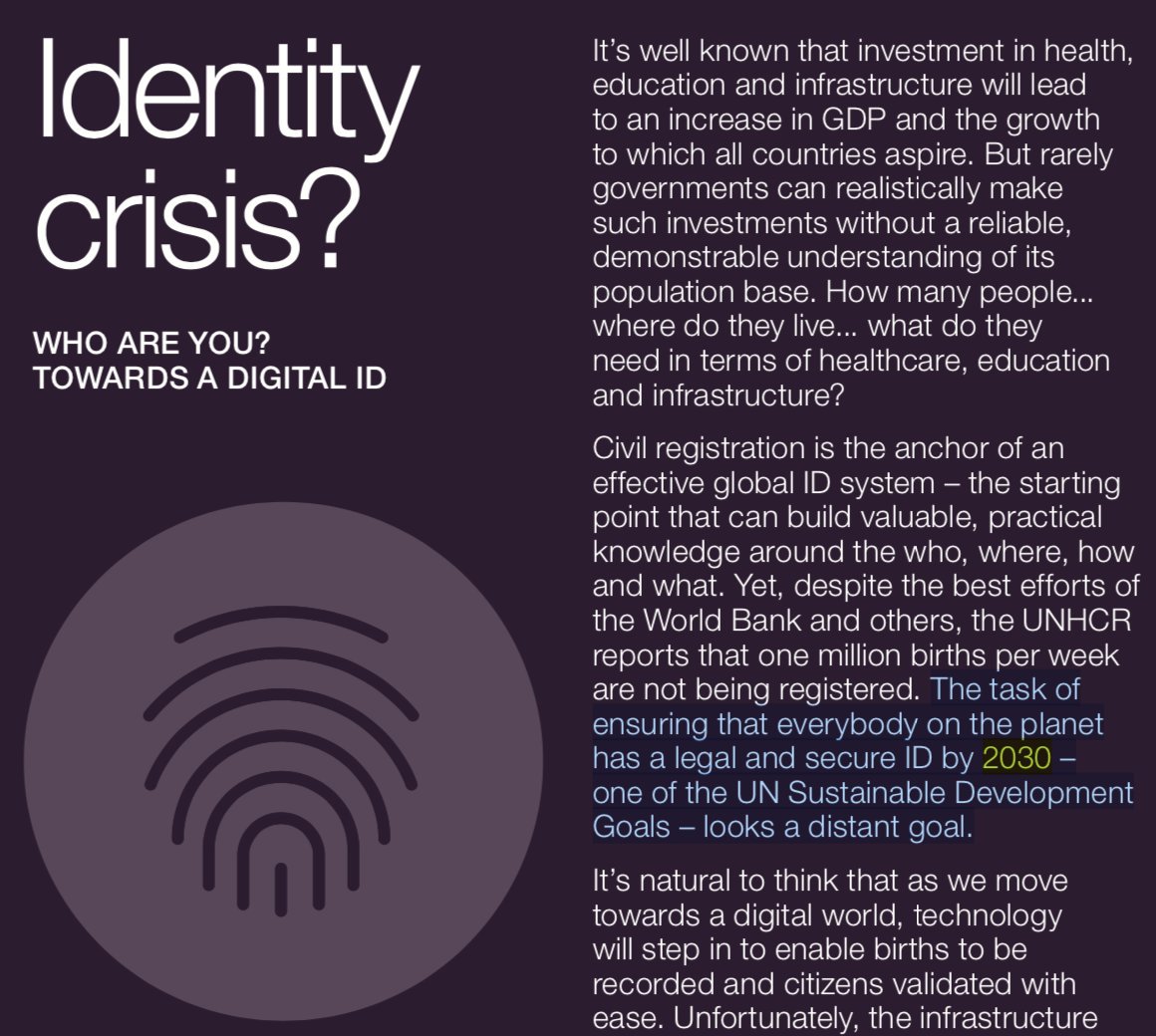

11 September 2017 (US-AID): IDENTITY IN A DIGITAL AGE: INFRASTRUCTURE FOR INCLUSIVE DEVELOPMENT

There may be no single factor that affects a person’s ability to share in the gains of global development -- to receive services and be represented -- as much as having an official identity. Identity is tied to voting rights, financial inclusion, land ownership, education, and can even help protect against human trafficking or child marriage. In many ways, the roughly 1.1 billion people who lack official identity are invisible, discounted, and left behind. Yet the complex political and social forces behind identity systems are often overlooked or misunderstood, leading to inefficiencies and missed opportunities for inclusive and sustainable ID systems...

ID2020

- ID2020 AN ALLIANCE COMMITTED TO IMPROVING LIVES THROUGH DIGITAL IDENTITY

- 20 December 2017 (ID2020) (ID2020) Davos 2018: Recap and Reflections

- 2 February 2018 (ID2020) Reflections and the Year Ahead

- 28 March 2018 (ID2020) Immunization: an entry point for digital identity

19 June 2017 (Reuters): Accenture, Microsoft team up on blockchain-based digital ID network:

Accenture Plc and Microsoft Corp are teaming up to build a digital ID network using blockchain technology, as part of a United Nations-supported project to provide legal identification to 1.1 billion people worldwide with no official documents.

Contactless

Contactless technologies (for payment especially) are part of the classic boiling-frogs strategy being implemented to soften us up to having microchip implants or e-skin/tattoos.

- Healthy Welfare Card: Architect of card, Andrew Forrest, says there should be no access to cash

- Contactless cards only work when all stakeholders back them — A Scandinavian study

- UK mobile contactless payments skyrocket

- Contactless cards and payment-enabled devices offer fast, easy and secure ways to pay. Here’s how they work.

- All age groups want contactless payment

- Wells Fargo Rolls Out Contactless Withdrawals At Thousands Of ATMs

- DERMALOG: Maldives Introduces Most Innovative ID Card (Derma - 'skin'!)

- Visa Brings Simple, Secure Payments to Garmin® vívoactive® 3 Smartwatch

- Mastercard Enables Garmin Users To Run and Shop At A Perfect Pace

Try contact-less for yourself

Contactless technology is in your pocket if you've got an Android phone with wireless NFC support built-in.

- Read your own debit/credit card with Credit Card Reader NFC (EMV) by Julien MILLAU https://play.google.com/store/apps/details?id=com.github.devnied.emvnfccard&hl=en_US

- Read your own passport with ReadID - NFC Passport Reader by InnoValor https://play.google.com/store/apps/details?id=nl.innovalor.nfciddocshowcase

Biometrics

Contactless will inevitably lead to biometrics as authorities and big-business intend to cajole us physically to consent to implementing The Mark of The Beast ourselves, voluntarily.

WEF: Empowering next-generation implantable brain interfaces (Timothy Constandinou)

- 9 May 2018 (NBC) Biometrics are here: The crazy ways you're going to be paying in the future

- VISA Security: Fighting fraud with a smile

Banco Neon + Visa use facial recognition - Electronic Skin Tattoo with RFID Technology to Facilitate Monitoring

- 13 May 2018 (SCMP) Thousands of people in Sweden get microchip implants for a new way of life Small implants were first used in 2015 in Sweden and since then people have become active in microchipping

AP: Swedish rail operator accepts microchip tickets

Wearable electronic skin:

Employee microchip implants raise ethical questions:

India - Aaadhaar

(Wikipedia) Aadhaar (English: Foundation) is a 12-digit unique identity number that can be obtained by residents of India, based on their biometric and demographic data.

- Unique Identification Authority of India (UIDAI)

- Indian Justice Minister: Aadhaar can't be misused

- Aadhaar database access found to be sold on WhatsApp for Rs 500; UIDAI official acknowledges major data breach

- The Hindu: Towards a database nation

- Aadhaar Has Created Serious Constitutional Anomaly. It Violates Fundamental Rights, Rule Of Law, Etc And Not Just Privacy Rights

- Activists have alleged that the girl died of starvation as her family’s ration card was cancelled as it was not linked to Aadhaar.

- Banks without Aadhaar enrolment centres to face Rs20,000 fine

- Video: India's Surveillance State

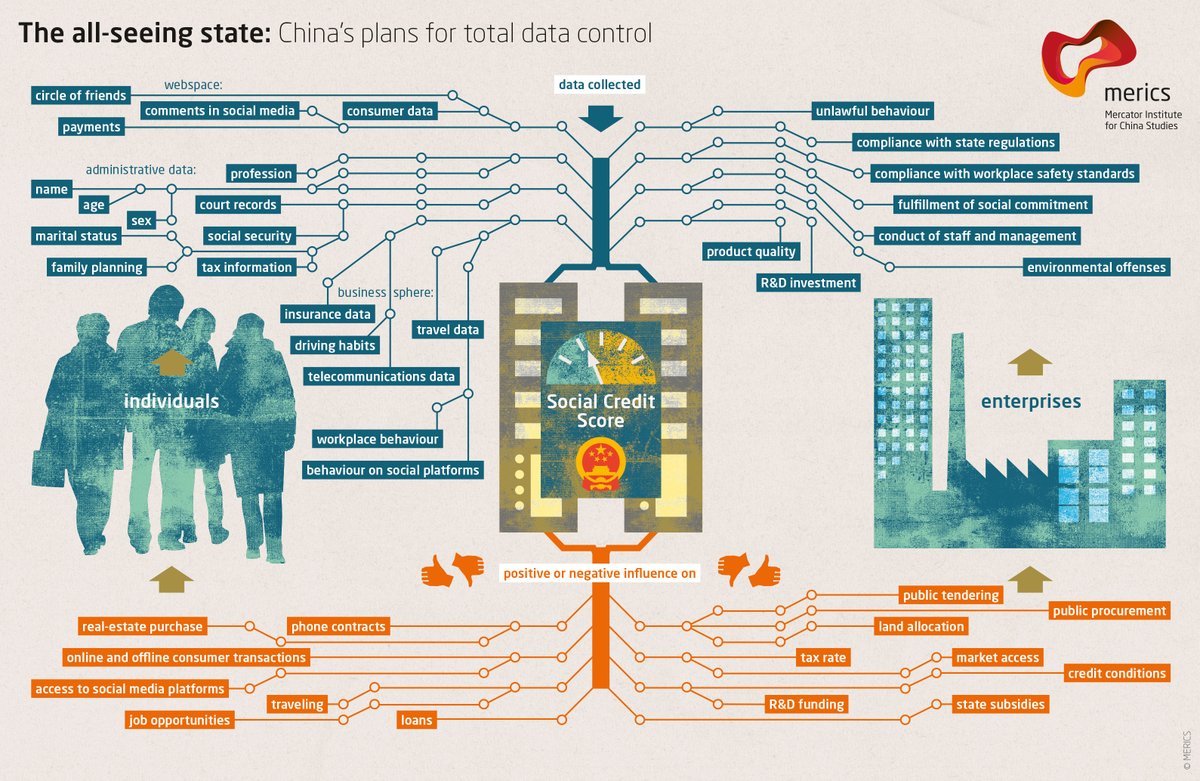

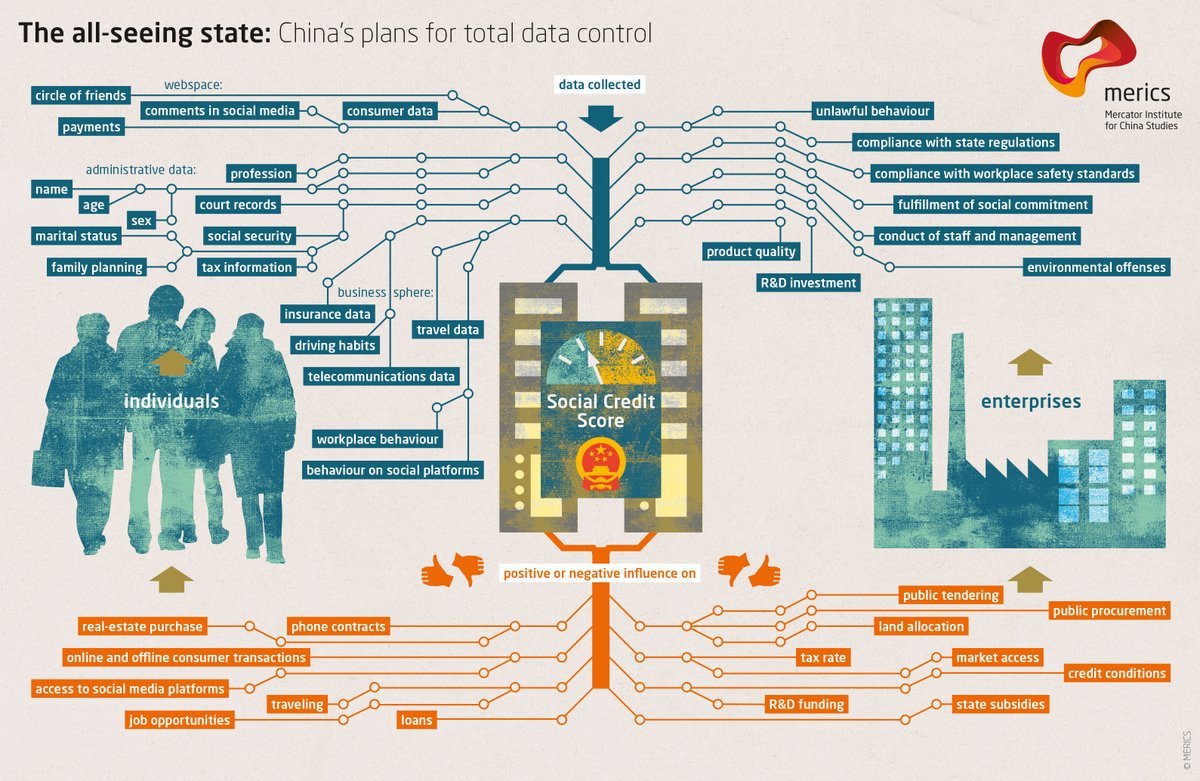

China - Social Credit

- Trust in Ratings: China’s Social Credit System

- The West could be closer to China's system of 'social credit scoring' than you think

- China’s Social Credit System Puts Its People Under Pressure to Be Model Citizens

- China will ban people with poor ‘social credit’ from planes and trains

- China bans journalist from buying a home due to “social credit score” system that punishes anyone who questions the state

- The odd reality of life under China's all-seeing credit score system

- China’s Big Brother reboot

The concept of privacy is set to vanish in the country - Video: China's AI facial recognition programme

Download China's Social Credit (diagram)

{kind=link}

The End Game

Governments, big-business, financial institutions and 'elites' of Davos who publish via the World Economic Forum are heavily promoting:

- Distributed Ledgers

- Microchip Implants

- Biometric Identification

- Basic Income

- Driverless Cars

- Robots replacing people in workplaces

- A future of renting (no more ownership!)

What would have seemed impossible even a generation ago is now becoming realised. A globally distributed identity database maintaining records on each and every individual is already being built. Digital currencies are being created and using ledgers where every transaction that takes place is recorded and can be monitored in real-time.

In the worst case scenario the social-credit system of China and biometric database and associated technology of India's Aadhaar will be rolled-out to the rest of the world. Universal Basic Income (UBI) will be provided as a bribe to get people to register their identity, initially with contactless technology and eventually obtain their unique biometric data. UBI will stop being 'universal' when it becomes means-tested by means of a citizens social credit score. People who refuse to participate in such schemes will not be able to opt-out of the financial system because cash transactions will be increasingly limited or eliminated through demonetisation and restrictions on cash for all but the smallest of purchases. By 2030, nobody will be able to opt-out as the UN goals for digitally registering all births around the globe are met. Our ability to move freely, travel long AND short distance will be impacted, civil liberties will be further eroded, no group of people will be able to assemble together without alerting 'authorities' through their digital footprint.

Do I have a wild imagination? Well, it's better than having NO IMAGINATION!

This is just the tip-of-the-iceberg of what kind of tyranny can occur if we do nothing. Paying in physical cash anonymously and privately is one of the few remaining liberties we have left today.

Social Implications

It should be obvious by now that making society cashless is so much more than just eliminating the way that we make payments. There are many implications beyond the tired old government tropes of stamping out crime and money-laundering, tax-avoidance, theft and so-on. Power and profit come into it, but it's ultimately about CONTROL; of you, I and everyone else on this planet.

The digital society requires a reliable and robust infrastructure, much of the developing world in particular are yet to have the permanent high-speed internet connections and reliable electricity supply that the developed nations take for granted. (Will the usual suspects (IMF/World Bank) be funding e-infrastructure projects and then pulling their old 'economic hitman' tricks or will the new AIIB?) What happens when there's a major system failure and there's no option to pay with cash?

Biometrics are not fool-proof. Fingerprints can be retrieved from a smooth surface, iris templates can be extracted from high resolution photos, video and voice recognition systems can be fooled by recordings and new software. Surveillance systems can identify people with or without their consent. People leave digital footprints wherever they go, online or offline, Artificial Intelligence systems can be used to help identify them. Should they be collecting this data? How long should it exist for? Who should have the right to access it and why? Will citizens have a right to access their digital profiles? Digital profiles can be used to target members of society for their political views. What are the other possible 'unintended consequences'? How much do we trust organisations with our data?

The leading currency printer (one of just a handful globally) De La Rue's annual report reiterated "The task of ensuring that everyone on the planet has a legal and secure ID by 2030" by UNHRC's 'Sustainable Development' goals. Should we even be have a digital ID? Why shouldn't we have a choice instead of being opted-in at birth? Davos's World Economic Forum tells us 5 predictions for what life will be like in 2030.

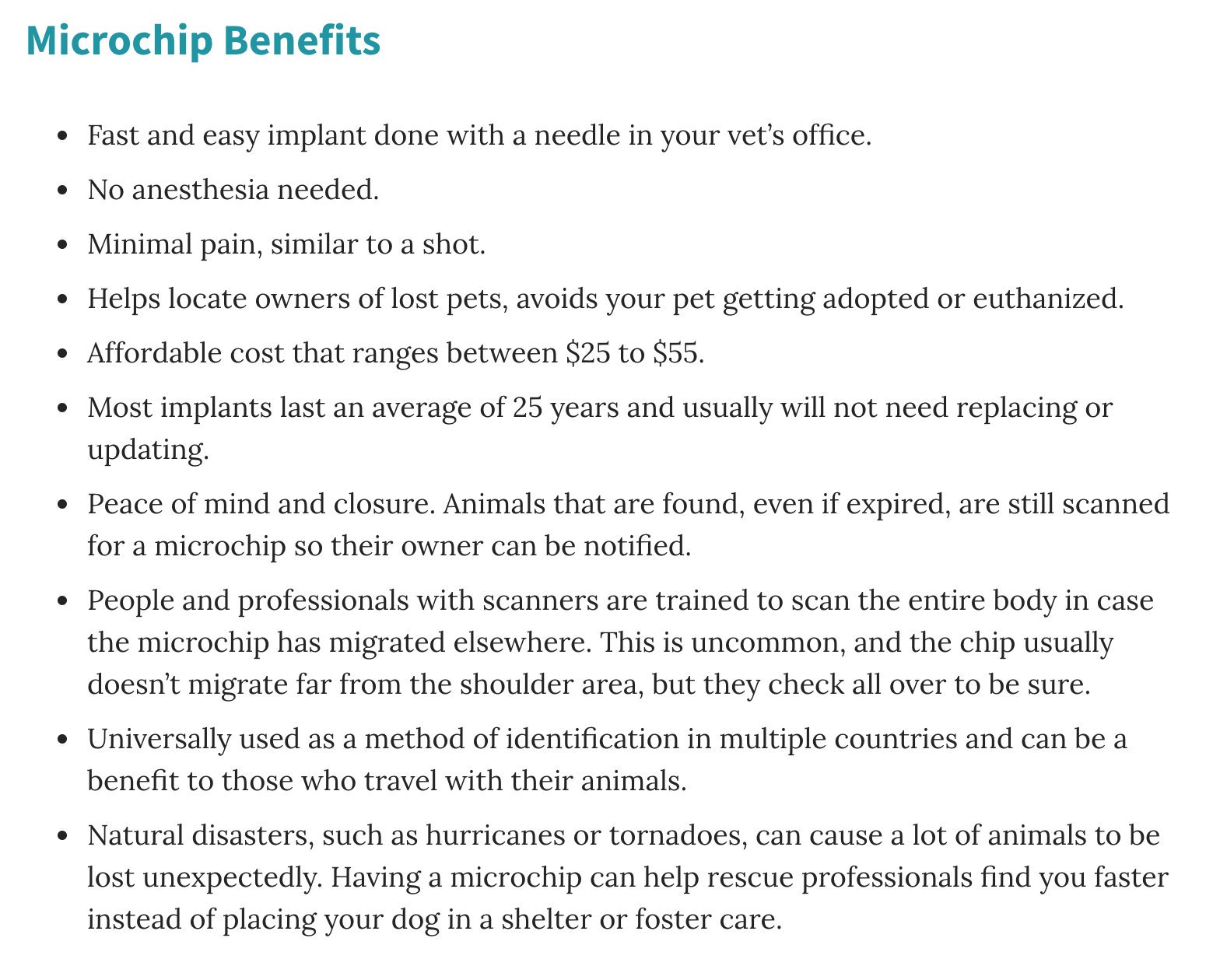

Is humanity being softened-up and encouraged to become pets like our dogs? How Does a Dog Microchip Work?

Find out the details and why you should consider getting one.

On an even more sinister level, the technological developments, media and cultural engineers are championing their use for transhumanism, body modifications and extensions 'to improve' our natural attributes. Do we want to 'evolve' in such antinomian ways?

In recent generations homosexuality has been normalised in The West for children, and transgenderism is now the next cultural and social taboo being pushed onto us by elites (why are governments and banks pushing homosexuality and transgenderism in the name of 'diversity'?). It's no longer science fiction to see that Sperm cells can be grown from human skin and animals like sheep can be grown outside the womb. Are they signalling an end to the time of natural and traditional families made of people born from mothers? Will we (continue to) be farmed, manipulated, controlled and kept-asleep from cradle-to-grave (albeit in the future as in The Matrix movies)?

Do we want everything in our homes to become a part of "The Internet Of Things (MS)" and for everything outside to become 'smart' including our urban environment? Do we want the likes of Microsoft CityNext and Google Sidewalk Labs to be planning our cities and how we live in them?

- Toronto Mayor expresses concern over Google’s new ‘digital city’

- Smart Cities

- Google Takes Big Data To Smart Cities

Are these new technologies even safe? There have been numerous warnings for example about 5G and health, not to mention more nefarious uses. What can we do in the face of messages like "Ready or not, 5G is coming?"

Finally, it's important to understand that our financial system is buit on dishonourable debt which is not viable long-term as national government debts mount and the total (including 'private' sector) world debt is is in the region of at least $230 trillion. Do we still need central banks? Even further still, maybe it's time we rethink our money altogether?

16 June 2018 - Bilderberg and the Digital New World Order by Truth Stream Media:

Max Igan interviewed in 2017 discussing the coming digital changes and how cashless is at the core of it.

What can I/we do? Pushing Back

- Use cash wherever and whenever possible.

- Tell your family and friends to do the same, and pay it forward.

- Write to your politicians, sign petitions, make your voice heard.

- Actively follow central banks, banks, and big-business, financial leaders and politicians on social media and watch their communications, and say what needs to be said.

- Tell everyone Cash Is Cool

- Keep up-to-date with Cash Essentials

- Take a look at the Global Yes To Cash movement or start your own!

- Get an ATM at your business with, e.g. YourCash

- Where possible, remove consent, don't unnecessarily volunteer your personal data and information. Make your data trail as minimal as possible.

Further Information

You'll see below that it's not all doom & gloom for cash and that it's even actually growing in places, but we need to be ever vigilant and make sure that it is never sidelined or eliminated because the day that happens will be the day we lose our freedom.

- e-estonia: we have built a digital

society and so can you Named ‘the most advanced digital society in the world’ by Wired, ingenious Estonians are pathfinders, who have built an efficient, secure and transparent ecosystem that saves time and money. e-Estonia invites you to follow the digital journey. - Book - Spychips - How Major Corporations & Government Plan To Track Your Every Move With RFID (2005) By Katherine Albrecht & Liz Macintyre

- Video: Brett Scott - Who Is Driving Cashless Society?

- NEVERMIND GUARANTEED INCOME, WE WANT THE COW

- The Perfect Robbery, The Cashless Society

- The End of Cash? Beware sleepwalking into a world without hard currency

- Bangladesh - Digitising Wage Payments in Bangladesh’s Garment Production Sector

- NO CURRENCY FOR OLD MEN

- Electronic money is for criminals and fraudsters, not cash! "Among those money mule transactions, more than 90% were linked to cyber-related crimes, such as phishing, online auction fraud..." so why all the discussion and actions to ban and reduce physical cash use in recent years? 159 ARRESTS AND 766 MONEY MULES IDENTIFIED IN GLOBAL ACTION WEEK AGAINST MONEY MULING

- "Cash is yet a dominant payment instrument in Japan, whereas its authorities cling more and more to cashless transactions, reports Euromonitor. According to the source, cash accounted for 62% of the total retail transactions last year." Cash Transactions Still Prevail in Japan

- "it is still the most widely used payment mechanism in the UK with cash in circulation growing by 10% in 2016, while in the USA growth is 7.5%, in the Eurozone 6%" Future of Cash Conference 2017 - Cash is popular, inclusive and growing strongly

- Why Technology Is Actually Helping Cash Thrive

- How a cashless society is boosting the fortunes of London's homeless

- UK banks ‘ditching the human touch’

- War on Cash intensifies: Citibank to stop accepting cash at some branches

- Debit cards overtake cash as top payment method Debit cards have overtaken cash to become the number one payment method in the UK, according to figures from the British Retail Consortium (BRC). The annual Payments Survey reveals that, for the first time, retail purchases made by card account for more than 50 per cent of all customer transactions by volume. (12/7/2017)

- THERE IS NO WAR ON CASH

- Australian Banks Demand Protection From Derivatives Losses Under Bail-In Plan

- Why Diversity in the Artificial Intelligence Sector Is Critical Mastercard vice chairman Ann Cairns also called attention to some of its existential risks.

- 12 June 2018 CITIBANK 10,000 JOBS COULD BE LOST TO ROBOTS SAYS CITI US bank Citi has warned that it could shed half of its 20,000 tech and ops staff in the next five years due to the rise of robotics and automation.

- WEF Dubai is introducing robotic policemen, to make up 25% of the force by 2030

- WEF This company replaced 90% of its workforce with machines. Here's what happened

- WEF Why Mark Zuckerberg is advocating universal basic income in the US

- WEF Would you let your employer implant a microchip in your hand? These workers have

- WEF A growing number of people think their job is useless. Time to rethink the meaning of work

- WEF A basic income could boost the US economy by $2.5 trillion

- WEF Creating a global crypto-currency, 4 Nov 2019

Independent research by the group Critical Thinking has also reached similar conclusions:

- War On Cash (and on us all) features a brief commentary about what I wrote here.

- Cashless Control

- Creeping Co-Option

Feel free to reproduce and remix this content providing that you insert a link back to here.